HOW YOUR INCOME WILL CHANGE NEXT WEEK

Millions of workers will see the impact of Stage 3 tax cuts in their next pay packet

By Bronwyn Allen

Fri, Jun 28, 2024 9:50am 2 min

2 min

2 min

Millions of workers will see the impact of Stage 3 tax cuts in their next pay packet

2 min

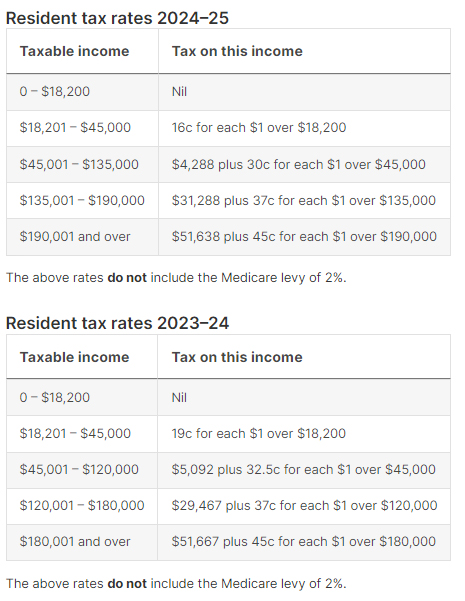

Stage 3 tax cuts will commence on Monday, providing 13.6 million workers with tax savings that they will see in their first pay packets of FY25. The average Australian wage earner on $74,500 per year will receive a $1,540 tax saving over the new financial year. The Superannuation Guarantee is also going up from 11 percent to 11.5 percent from Monday, providing the same worker with a $372 bump per annum to the superannuation payments they receive from their employer.

The Albanese Government amended the Stage 3 tax cuts in January to give every taxpayer a tax cut rather than only those on higher incomes. Many economists have argued the tax cuts will add to inflation, which is proving to be remarkably sticky. Yesterday, the Australian Bureau of Statistics released the May inflation figures showing a 4 percent annual increase in inflation, up from 3.6 percent in April.

The Federal Government decided to amend the legislated tax cuts in January to help more Australians with rising cost of living pressures. Official advice from the Federal Treasury said the amendments were “broadly revenue neutral” because they would cost almost the same amount as the original Stage 3 plan, which had already been factored into inflation forecasts. The amendments reduced the tax break for earners at the top end to enable tax relief for everyone. A Treasury document said the changes “will not add to inflationary pressures and will support labour supply”.

The tables below outline how the tax rates and tax brackets will change from Monday.

At a press conference after the Reserve Bank announced interest rates would remain on hold last week, Governor Michele Bullock said she expects some people would use their tax cuts to cover everyday expenses while others would save it.

“What we do observe in the data is that people who have mortgages – on average, not all – but people on average who have mortgages tend to try and put more into their offset accounts and their redraw facilities because they’re paying quite a high interest rate now on their mortgage and so they want to offset it,” she said.

A Westpac survey found Australians planned to save up to 80 cents for every $1 of tax savings.

“The results suggest consumers will use tax relief as an opportunity to repair their finances and rebuild saving buffers rather than spend,” said senior Westpac economist Matthew Hassan.

If taxpayers followed through on this plan, Mr Hassan said only $4.7 billion of the $23.3 billion in tax relief would be spent, equating to a spending boost of 35 basis points.

Rugged coastal drives and fireside drams define a slow, indulgent journey through Scotland’s far north.

A haven for hedge-fund titans and Hollywood grandees, Greenwich is one of the world’s most expensive residential enclaves, where eye-watering prices meet unapologetic grandeur.

The lunar flyby would be the deepest humans have traveled in space in decades.

4 min

It’s go time for the highest-stakes mission at NASA in more than 50 years.

On April 1, the agency is set to launch four astronauts around the moon, the deepest human spaceflight since the final Apollo lunar landing in 1972.

The launch window for Artemis II , as the mission is called, opens at 6:24 p.m. ET.

National Aeronautics and Space Administration teams have been preparing the vehicles to depart from Florida’s Kennedy Space Center on the planned roughly 10-day trip. Crew members have trained for years for this moment.

Reid Wiseman, the NASA astronaut serving as mission commander, said he doesn’t fear taking the voyage. A widower, he does worry at times about what he is putting his daughters through.

“I could have a very comfortable life for them,” Wiseman said in an interview last September.

“But I’m also a human, and I see the spirit in their eyes that is burning in my soul too. And so we’ve just got to never stop going.”

Wiseman’s crewmates on Artemis II are NASA’s Victor Glover and Christina Koch, as well as Canadian Space Agency astronaut Jeremy Hansen.

What are the goals for Artemis II?

The biggest one: Safely fly the crew on vehicles that have never carried astronauts before.

The towering Space Launch System rocket has the job of lofting a vehicle called Orion into space and on its way to the moon.

Orion is designed to carry the crew around the moon and back. Myriad systems on the ship—life support, communications, navigation—will be tested with the astronauts on board.

SLS and Orion don’t have much flight experience. The vehicles last flew in 2022, when the agency completed its uncrewed Artemis I mission .

How is the mission expected to unfold?

Artemis II will begin when SLS takes off from a launchpad in Florida with Orion stacked on top of it.

The so-called upper stage of SLS will later separate from the main part of the rocket with Orion attached, and use its engine to set up the latter vehicle for a push to the moon.

After Orion separates from the upper stage, it will conduct what is called a translunar injection—the engine firing that commits Orion to soaring out to the moon. It will fly to the moon over the course of a few days and travel around its far side.

Orion will face a tough return home after speeding through space. As it hits Earth’s atmosphere, Orion will be flying at 25,000 miles an hour and face temperatures of 5,000 degrees as it slows down. The capsule is designed to land under parachutes in the Pacific Ocean, not far from San Diego.

Is it possible Artemis II will be delayed?

Yes.

For safety reasons, the agency won’t launch if certain tough weather conditions roll through the Cape Canaveral, Fla., area. Delays caused by technical problems are possible, too. NASA has other dates identified for the mission if it doesn’t begin April 1.

Who are the astronauts flying on Artemis II?

The crew will be led by Wiseman, a retired Navy pilot who completed military deployments before joining NASA’s astronaut corps. He traveled to the International Space Station in 2014.

Two other astronauts will represent NASA during the mission: Glover, an experienced Navy pilot, and Koch, who began her career as an electrical engineer for the agency and once spent a year at a research station in the South Pole. Both have traveled to the space station before.

Hansen is a military pilot who joined Canada’s astronaut corps in 2009. He will be making his first trip to space.

Koch’s participation in Artemis II will mark the first time a woman has flown beyond orbits near Earth. Glover and Hansen will be the first African-American and non-American astronauts, respectively, to do the same.

What will the astronauts do during the flight?

The astronauts will evaluate how Orion flies, practice emergency procedures and capture images of the far side of the moon for scientific and exploration purposes (they may become the first humans to see parts of the far side of the lunar surface). Health-tracking projects of the astronauts are designed to inform future missions.

Those efforts will play out in Orion’s crew module, which has about two minivans worth of living area.

On board, the astronauts will spend about 30 minutes a day exercising, using a device that allows them to do dead lifts, rowing and more. Sleep will come in eight-hour stretches in hammocks.

There is a custom-made warmer for meals, with beef brisket and veggie quiche on the menu.

Each astronaut is permitted two flavored beverages a day, including coffee. The crew will hold one hourlong shared meal each day.

The Universal Waste Management System—that’s the toilet—uses air flow to pull fluid and solid waste away into containers.

What happens after Artemis II?

Assuming it goes well, NASA will march on to Artemis III, scheduled for next year. During that operation, NASA plans to launch Orion with crew members on board and have the ship practice docking with lunar-lander vehicles that Elon Musk’s SpaceX and Jeff Bezos’ Blue Origin have been developing. The rendezvous operations will occur relatively close to Earth.

NASA hopes that its contractors and the agency itself are ready to attempt one or more lunar landing missions in 2028. Many current and former spaceflight officials are skeptical that timeline is feasible.